The chemical sector alone is responsible for 2% of global anthropogenic CO2 emissions, and the industry depends heavily on finite fossil fuel feedstocks. The new IDTechEx report, “Carbon Dioxide Utilization 2024-2044: Technologies, Market Forecasts, and Players”, explores how captured CO2 could be utilized as a feedstock for hundreds of different chemicals instead. Valorizing waste carbon dioxide has already proven profitable in the chemicals industry for polycarbonate polymers. Overall, IDTechEx forecasts revenue from CO2-derived polymers and other drop-in chemicals will exceed US$47 billion in 2044.

Why is CO2 utilization in chemical production important?

Carbon capture is viewed as a key technology for achieving net-zero goals as it can decarbonize hard-to-abate sectors. However, carbon capture technologies are expensive, and regulatory pressure to decarbonize remains weak worldwide. If captured carbon can be utilized to make profitable chemical products, this revenue stream can provide an economic incentive to accelerate the uptake of CCUS (carbon capture, utilization, and storage) technologies until legislation that promotes CO2 storage emerges.

While many CO2-derived chemicals do not always represent net-negative or net-zero products, they do still represent reductions in emissions compared to the fossil fuel-based status quo and should not be overlooked as a decarbonization tool.

For more information on capturing CO2, particularly for hard-to-abate sectors such as cement, please refer to the “Carbon Capture, Utilization, and Storage (CCUS) Markets 2023-2043” market intelligence report.

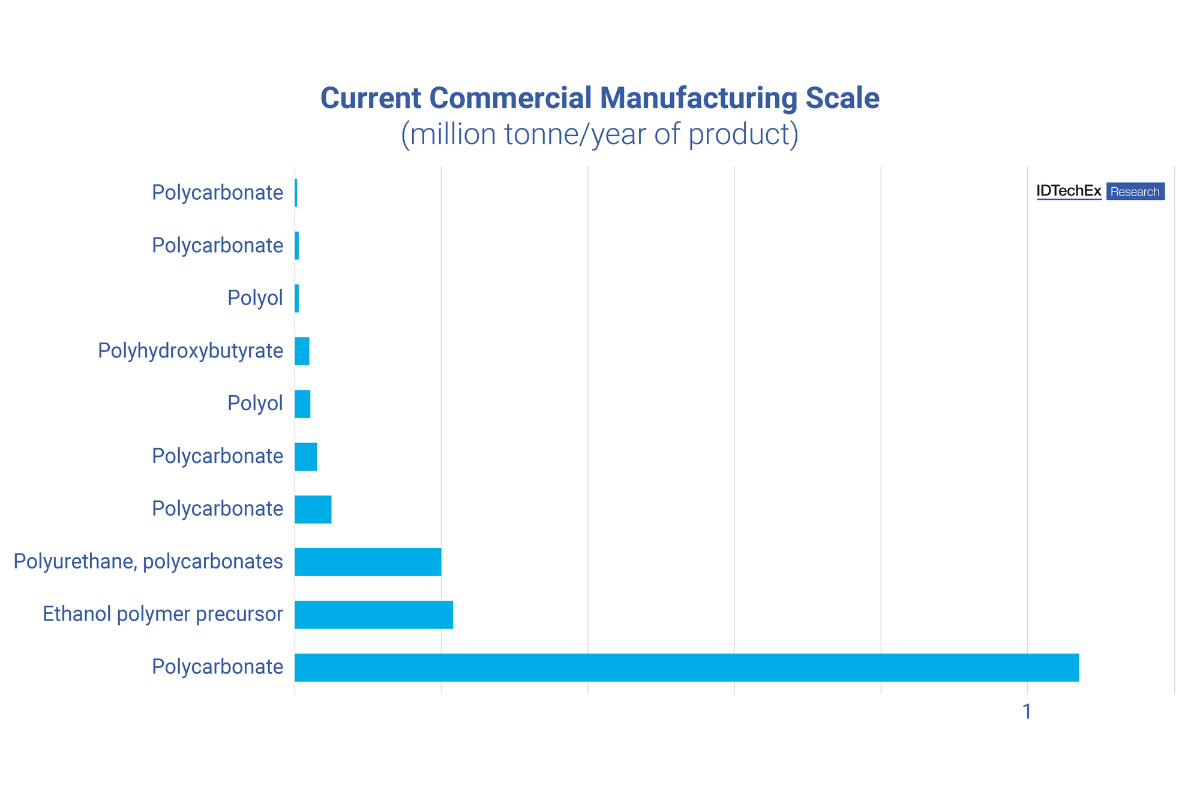

CO2 utilization in chemicals is already profitable

Utilizing captured CO2 to make chemicals is not a far-fetched fantasy. Profitable production of CO2-derived polymers has quietly been around for decades. One of the pioneers was Asahi Kasei, which commercialized a process making aromatic polycarbonates from waste CO2 in 2002. Since then, the total annual production capacity of polycarbonate resin using this technology has reached about 1 million tonnes.

Similarly, Aramco Performance Materials has developed polycarbonate polyols (‘Converge’ polyols) containing up to 40% CO2, which can be used in industrial applications, including coatings and foams. In January 2024, Aether Industries, H.B. Fuller, and Saudi Aramco Technologies announced the commercialization of these polyols. Moreover, German materials company Covestro uses CO2 to produce polycarbonate and isocyanate (polyurethane precursor), and UK-based Econic Technologies recently unveiled new technology for memory foam mattresses based on captured CO₂ emissions.

High CO2 prices can be tolerated using these methods, and players have reported improved material performance. However, the product volumes and the CO2 utilization ratio in polymer manufacturing are relatively small, limiting its CO2 utilization potential. Production growth is, therefore, likely to continue to be driven by superior performance instead of CCUS regulation or voluntary carbon credits.

The existing routes to CO2-derived polymers and polymer precursors all generally rely on the same simple chemical idea: break as few strong carbon and oxygen bonds in CO2 as possible. This non-reductive approach results in a lower energy demand and, crucially, no clean hydrogen requirements.

The hydrogen bottleneck

But what about making chemicals containing many hydrogen-to-carbon bonds? Currently, clean hydrogen production is expensive and can raise costs significantly compared to fossil-based chemicals. Green hydrogen economics are only expected to improve significantly in the 2030s (driven by reductions in the price of renewable energy and improvements in electrolyzer technology), but chemical production from captured CO2 and H2 should not be written off completely in 2024.